By BIll Studebaker, CIO & President, ROBO Global

Navigating an environment where good news turns to bad news and soft landings become ‘no landings’ (quicker than we can even take notes) feels like taking a test we haven’t studied for. It’s exhausting.

Even the teachers (the Federal Reserve) don’t seem to have the answers in hand! Recent manufacturing purchasing managers' index (PMI) prints in the US (47.8 vs. 47.1 cons), UK (49.2 vs. 47.5 cons), and Europe (52.3 vs. 50.6 cons) all point to the simple fact that the global economy remains far more resilient than most expected. Which begs the question: where do we go from here?

For context, the close of a rocky February spurred a flurry of discussion around the type of economic ‘landing’ in our future. A soft landing (the ideal) is one where recent rate hikes effectively slow the economy just enough to dampen demand and inflation—without deflating the GDP or increasing unemployment. A hard landing (which everyone wants to avoid!) is, of course, a full-blown recession and the unemployment numbers that go hand in hand with a tumbling economy. Then there’s the newest buzzword—‘no landing’—which is when, despite rate hikes and rising inflation, the economy continues to accelerate. Consumers keep shopping. Homebuyers keep buying. Companies keep hiring. The result: the plane never hits the ground. The economy keeps flying and, to rein it in, the Fed keeps hiking rates, creating one more conundrum for consumers and investors alike.

Looking at today’s rather bizarre economy, I have to wonder if the whole airplane metaphor is misguided. Maybe Captain Powell isn’t flying a plane, but rather a new sort of ship that can stay in the air far longer, flying us into uncharted territory. If we’re not on the brink of a global recession (which certainly seems to be the case), I think now is the time to lose the metaphors and focus on the fundamentals and facts.

Let’s start with the numbers. The month of February delivered a welcome dispersion of returns for the ROBO Global indices. The ROBO Global Artificial Intelligence ETF (THNQ) gained +1.59%, while the ROBO Global Robotics and Automation Index ETF (ROBO) pulled back -1.32%, and the ROBO Global Healthcare Technology and Innovation ETF (HTEC) declined -4.57%. [1]

Now for the details:

#1: Automation is no longer a luxury.

As we have been reminding investors for years, in our opinion automation has become an absolute necessity. This fact was exacerbated by the pandemic which altered consumer habits, increased consumer expectations, and put pressure on companies to increase margins and accelerate their supply chains. The rate of adoption for automation has continued to accelerate. There are green shoots virtually everywhere, including in M&A which is always in play. Just one example: medical equipment maker Danaher (DHR) has expressed interest in taking over contract drug maker Catalent (CTLT), an HTEC portfolio company. While a deal isn’t imminent, Danaher’s overtures have valued the manufacturer at a significant premium, underscoring the urgency to automate. Across our constituents, we are seeing record levels of order backlogs and increased momentum—despite the fear of recession and a rocky stock market.

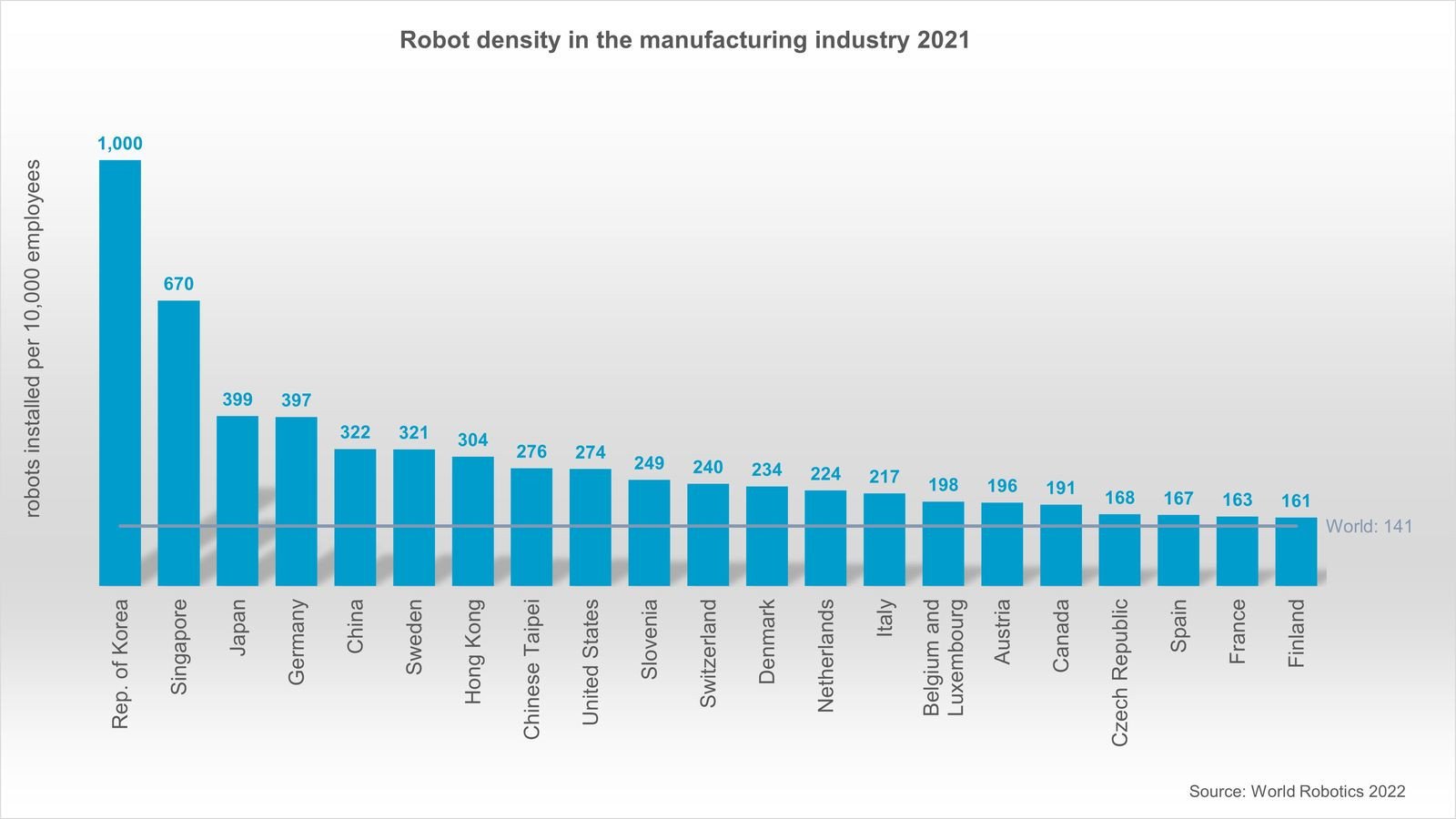

#2: China's manufacturing activity and automation adoption is expanding.

The official manufacturing purchasing managers’ index released on Wednesday showed that China’s manufacturing activity in February expanded at the fastest pace in more than a decade. The expansion smashed expectations, with production zooming after the lifting of COVID-19 restrictions late last year. China surpassed the US in robot density for the first time in 2022[i]—a key indicator of the country’s automation adoption in the manufacturing industry. At the same time, PMI shot up to 52.6 from 50.1 in January[ii], surpassing the 50-point mark that separates activity expansion and contraction. The PMI far exceeded an analyst forecast of 50.5 and was the highest reading since April 2012.

#3: The White House is pushing for automation of US ports.

Labor unions have rallied against automation adoption for decades, but it seems a tipping point may have finally arrived. The use of port automation has been a key sticking point in the negotiations between the International Longshore and Warehouse Union (ILWU) and the Pacific Maritime Association (PMA), and that resistance has slowed adoption at a point in the supply chain that needs it most: the ports. That may change quickly following comments by White House supply-chain envoy Stephen Lyons at the TPM23 Conference in Long Beach who stated that “the US ports and logistics industry needs to embrace automation in order to improve efficiency.” Speaking at the TPM23 Conference, Lyons stressed that automation was “inevitable” and that the industry should “move there deliberately as opposed to getting dragged.”

I could go on, but I’ve made my point. Whether Captain Powell steers us to a soft landing, a hard landing, or no landing at all, we believe automation is vital to the success of the global companies that will ultimately drive the economy forward. If you’re an investor who wants to ensure a graceful landing of your own ‘plane’ in the years to come, investing in robotics, automation, and healthcare technologies may just be the perfect ‘landing gear’ to have on board.

[i] According to the World Robotics 2022 report, presented by the International Federation of Robotics (IFR)

[ii] According to China's National Bureau of Statistics

ROBO Top Ten Holdings, HTEC Top Ten Holdings, THNQ Top Ten Holdings

SOURCES:

[1] Source: ROBO Global®, S&P CapitalIQ, For standardized performance data current to the most recent month end, please visit www.roboglobaletfs.com.

The performance data quoted represents past performance and is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when sold or redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data quoted. Holdings are subject to change. Indices are unmanaged and do not include the effect of fees. One cannot invest directly in an index.

This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the fund or any security in particular. Please consult your financial advisor for further information.

{kind=link}

Carefully consider the Funds’ investment objectives, risk factors, charges and expenses before investing. This and additional information can be found on the Funds' full or summary prospectuses, which may be obtained at www.roboglobaletfs.com. Read the prospectus carefully before investing.

Investing involves risk, including the possible loss of principal. International investments may also involve risk from unfavorable fluctuations in currency values, differences in generally accepted accounting principles, and from economic or political instability. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Narrowly focused investments and investments in smaller companies typically exhibit higher volatility. There is no guarantee the funds will achieve their stated objective. ROBO and HTEC are diversified. THNQ is non-diversified.

The liquidity of the A-shares market and trading prices of A-shares could be more severely affected than the liquidity and trading prices of other markets because the Chinese government restricts the flow of capital into and out of the A-shares market. The funds may experience losses due to illiquidity of the Chinese securities markets or delay or disruption in execution or settlement of trades.

The risks associated with investments in Robotics and Automation Companies include, but are not limited to, small or limited markets for such securities, changes in business cycles, world economic growth, technological progress, rapid obsolescence, and government regulation. Robotics and Automation Companies, especially smaller, start-up companies, tend to be more volatile than securities of companies that do not rely heavily on technology. Rapid change to technologies that affect a company's products could have a material adverse effect on such company's operating results. Robotics and Automation Companies may rely on a combination of patents, copyrights, trademarks and trade secret laws to establish and protect their proprietary rights in their products and technologies. There can be no assurance that the steps taken by these companies to protect their proprietary rights will be adequate to prevent the misappropriation of their technology or that competitors will not independently develop technologies that are substantially equivalent or superior to such companies' technology.

The risks associated with Artificial Intelligence (AI) Companies include, but are not limited to, small or limited markets, changes in business cycles, world economic growth, technological progress, rapid obsolescence, and government regulation. Rapid change to technologies that affect a company’s products could have a material adverse effect on such company’s operating results. AI Companies also rely heavily on a combination of patents, copyrights, trademarks and trade secret laws to establish and protect their proprietary rights in their products and technologies. There can be no assurance that the steps taken by these companies to protect their proprietary rights will be adequate to prevent the misappropriation of their technology or that competitors will not independently develop technologies that are substantially equivalent or superior to such companies’ technology. AI Companies typically engage in significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful.

The risks associated with Medical Technology Companies include, but are not limited to, small or limited markets for such securities, changes in business cycles, world economic growth, technological progress, rapid obsolescence, and government regulation.

Diversification may not protect against market risk.

Beginning September 2, 2020, market price returns are based on the official closing price of an ETF share or, if the official closing price isn't available, the midpoint between the national best bid and national best offer (“NBBO”) as of the time the ETF calculates current NAV per share. Prior to September 2, 2020, market price returns were based on the midpoint between the Bid and Ask price. NAVs are calculated using prices as of 4:00 PM Eastern Time. The returns shown do not represent the returns you would receive if you traded shares at other times.

The Funds are distributed by SEI Investments Distribution Co. (SIDCO) 1 Freedom Valley Drive, Oaks, PA, 19456